The Basics of Blockchain: A Simple Guide to Understanding | Bulls and Apes Project

Nov 03, 2022If you’ve become familiar with cryptocurrency or have spent any time exploring Web3, you’ve no doubt interacted with the blockchain. You’ve probably heard how this technology will be one of the most massive changes in the world. But let’s be honest- at some point, you’ve probably wondered, “What exactly is the blockchain?” Let’s get into a simplified explanation to help understand this technology.

What is a blockchain?

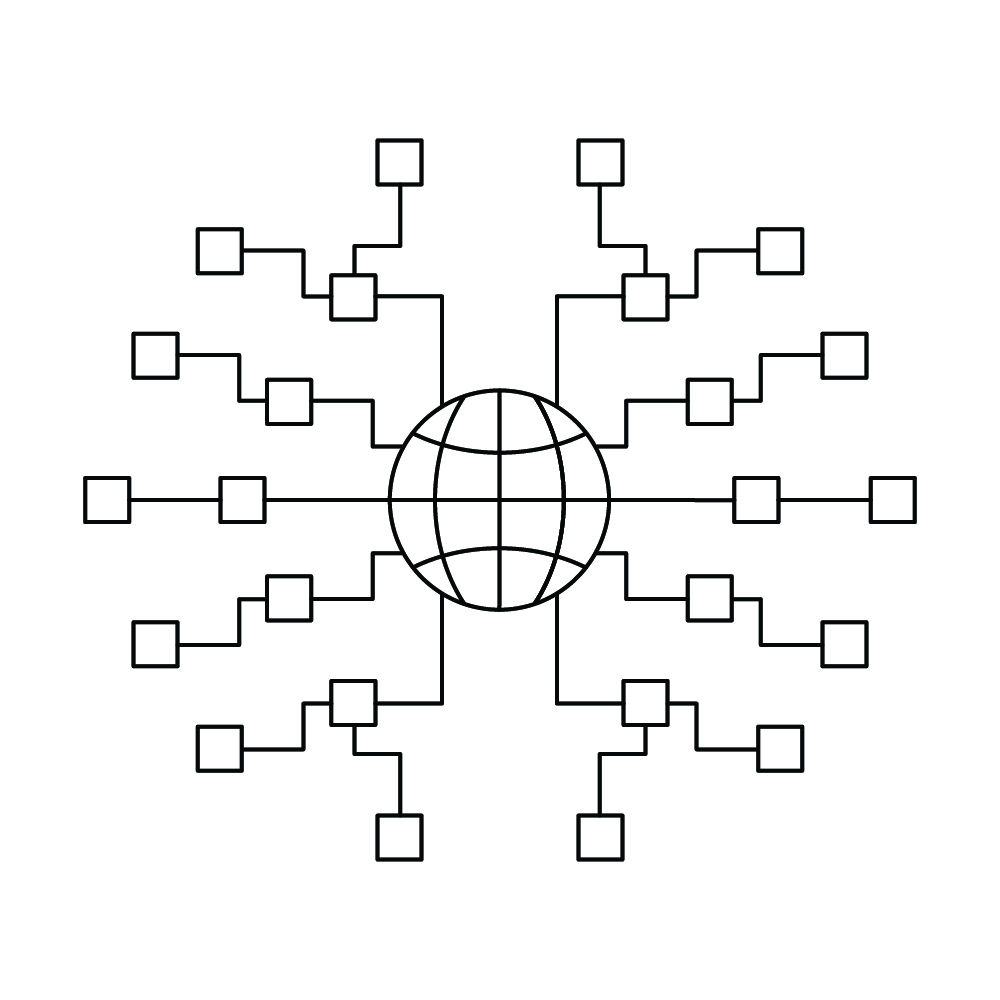

The blockchain is a digital database carrying information that can be used and shared concurrently within an expansive, decentralized network accessible to the public.

That might sound confusing, but it isn’t as complicated as it may seem. Let’s use the analogy of electronic payments since we’ve all used banks and most likely use electronic forms of payment rather than cash.

Say you’re buying something from your favorite online store. You enter your bank card number for the payment. As the payment processes, the website you’re buying from sends a message to your bank. Your bank checks to make sure you have enough money in your account. Your bank confirms that you have enough money in your account, lets the website’s bank know they can have the funds from your account, and approves the transaction. Then, your bank sends over the money from your bank account to the website’s bank account. The bank deducts the funds from your bank account and credits the website’s bank account. This transaction records in both your bank and the website’s bank electronic ledgers, and you both count on the bank to make sure they’re doing this correctly. These transactions happen throughout each day, and each bank diligently tallies all of the funds going in and out of customer accounts in their electronic ledgers in almost real-time. We count on banks to run this smoothly, and they have done a (mostly) good job for hundreds of years.

With the rise of technology, the documentation of financial transactions between two people or businesses can now occur on the blockchain. Instead of transactions between private banks like your bank and the website’s bank, all transactions are recorded publicly on the internet. The blockchain verifies these transactions.

Using the example of shopping at your favorite online store, let’s say you’re now using cryptocurrency rather than the money in your bank account to purchase your items. Instead of the bank confirming that you have the funds in your account to approve the transaction, the transaction runs through a vast public network. On this network, there are computers all around the world keeping track of every single transaction taking place. If you don’t have enough crypto in your wallet (akin to your bank account), all the computers will note the discrepancy in your wallet balance and reject the transaction. If you do, in fact, have enough crypto in your wallet, they’ll approve the transaction and record it into the public record on the blockchain. Everyone viewing this public network can see the transaction and confirm the crypto transferred from your crypto wallet into the shopping website’s crypto wallet.

How is the blockchain constructed?

Remember when I told you that this was a simplified explanation of the blockchain? Please keep that in mind as we continue because the blockchain is much more complex. It handles millions of users the world over, so its construction and design are intricate. With that, let’s get into the simple explanation.

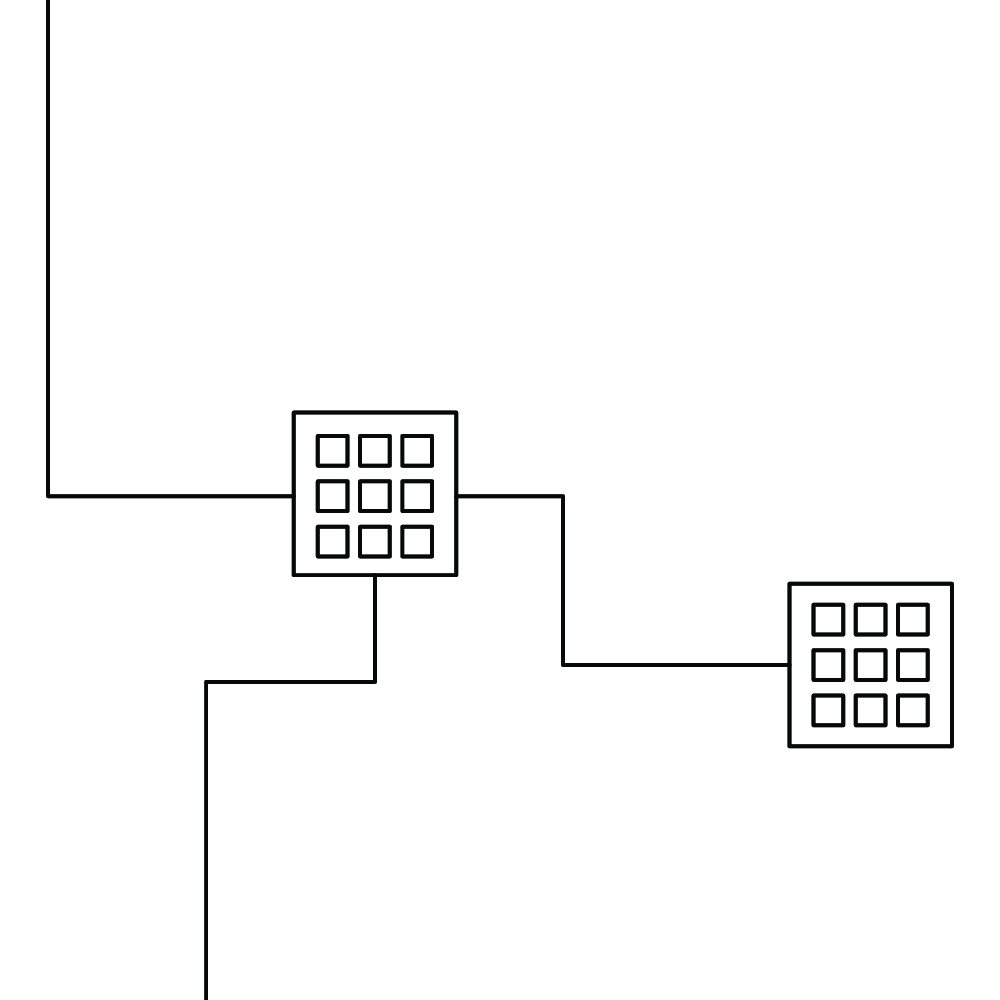

The blockchain begins with blocks or the components that store data on the blockchain. You’ll find that anyone can create a block to store any data they want.

When NFT project creators create a block, they create a smart contract or encoded instructions to act as a tool to carry out a sales agreement. For cryptocurrency, holders can transfer coins from one wallet to another, and the blockchain notes all receipts for these transactions.

If you decide to create on the block, and then create a second block, the second would line up after the first. As people generate more blocks, the blocks line up next to the block before them, and so on. The result is a chain of blocks. Each block stores specific data on its determined blockchain platform. Ehtereum, for example, is a blockchain platform.

When new blocks are accepted and added to the blockchain, it’s nearly impossible to remove them. However, new blocks are much easier to add. Blocks have limited storage capacity; when filled, they close and link to the block filled before it. All the fresh, new data is entered into a new block, and that block becomes part of the chain. When each block fills, the data is immortalized and melds into its timeline. Blocks are issued a timestamp to note the precise time the block becomes part of the timeline.

How is the blockchain decentralized?

The traditional forms of centralized record-keeping maintain transactions in one place. Think of home ownership records. You can typically track this information with your local municipalities. The municipality keeps track of the dates of sale and tracks ownership in its ledger. The municipal organization maintains these records in one specific place.

In contrast, the blockchain was designed to be distributed among a vast network of computers or decentralized. This makes data tampering more difficult and creates trust in the data by verifying and sharing some information. Blocks added to the chain must be verified and shared with other computers in the network. This is called proof of work. If the network of computers can verify this proof of work, the block can be added to the chain. The process of the network verifying and sharing this information ensures that each block is trustworthy. Users can then interact with their data in real-time.

Traditionally, when people wanted to purchase real estate or something high-value, they worked with a bank or broker to review records and maintain our confidentiality. The banks or brokers were the trusted “middlemen” and limited potential risk in the transaction. This added step cost time and money. If home ownership records were stored on a blockchain, it would alleviate the need for middlemen to confirm information. Since all of the blocks added to the chain are verifiable and cannot be tampered with, the transfer of ownership can be verified by simply showing the purchasing party the ownership data on the blockchain. Time and money can be conserved.

You can see how this trusted peer-to-peer interaction with data opens up all new methods to access, verify, and transact with others. Blockchain mechanics can be implemented in many ways since it’s a type of technology rather than a single network. Some blockchains can be entirely public for anyone to view and access, while others can be closed to an authorized group of users. There can also be hybrid public/private blockchains as well. In some, those with private access can view the data in its entirety, while the public can view selected data. In the NFT space, transactions are open for public view, and due to this transparency, anyone can view ownership transfers.

The combination of decentralized data, trust built into the data confirmation process, and the users’ ability to directly interact with their peers and the data, give blockchain technology the potential to change many of the ways we interact with one another.

Where do we go from here?

Blockchain technology is gaining notoriety because of its application practicality. Its transparent accuracy, efficiency, cost-effectiveness, security, and lack of outside engagement are appealing. Currently, we see many NFTs and asset tokenization on the blockchain. As more individuals and entities realize blockchain technology’s potential uses, we are sure to see its uses expand into many new forums.

It’s an exciting time to evaluate how digital assets are held on the blockchain. NFT projects, like The Bulls and Apes Project, are on the cutting edge of using blockchain technology to conduct their transactions. There is much more to the technology that you can explore and you’ll want to keep an eye on what’s happening with innovation on blockchains as you map out your business strategy.

For more information about blockchain and web3 technology check out our free NFTs 101 course!

Don't Miss Another Update!

Join our mailing list to be the first to find out when a new VC Deal drops, project utility updates, announcements and more!

We hate SPAM. We will never sell your information, for any reason.